PRINCE2 2009 - Directing Projects with PRINCE2 part 21

of the Cabinet Office under delegated authority from the Controller of HMSO.

Starting up a Project

Prepare the outline Business Case

© Crown copyright 2005 Reproduced under licence from OGC

In project management it is all too easy to concentrate on what has to be done and how it should be done, while overlooking why it needs to be done.

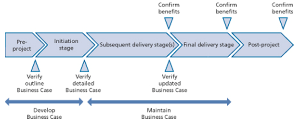

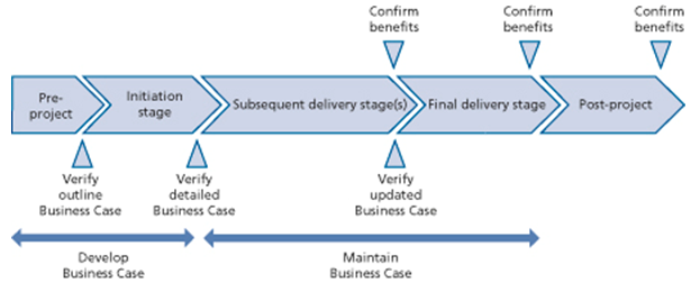

The Business Case defines why the work needs to be done and, as such, provides a crucial baseline for the project (see the diagram).

In PRINCE2, the Business Case is developed at the beginning of the project and maintained throughout the life of the project, being formally verified by the Project Board at each key decision point, such as end stage assessments, and confirmed throughout the period that the benefits accrue.

Note that the responsibility for confirming benefits post-project needs to be transferred from the Project Board to corporate or programme management when closing the project.

The Executive is responsible for the Business Case and therefore its development.

This does not necessarily mean that the Executive writes the Business Case: the responsibility is to ensure that it is written and to underwrite its content.

Preparing the Business Case may be delegated, for example, to a business analyst or to the Project Manager (if they possess the appropriate business skills).

Given the often relatively scarce information available at this point, the Business Case is likely to have a high-level perspective at this time, and will need to be refined during project initiation.

Nevertheless, sufficient time [see 'The Complete Time Management package'] should be allowed for developing, reviewing and approving the outline Business Case because:

- It is the most important control in the project. It drives the decision-making processes and is used continually to align the project’s progress to the business objectives and benefits that have been agreed

- It justifies the project effort, based on the estimated costs, the risks involved and the expected business benefits

- It covers the entire scope of business changes being introduced by the project (e.g. the cost of introducing new equipment should include the impact on personnel, training, changed procedures, accommodation changes, operational costs, relationships with the public etc.)

The outline Business Case is based on costs and timescales that are at best approximate.

Once the costs and timescales are better understood the viability may increase or decrease - perhaps resulting in the need to change the selected business option. Accordingly, it is often wise to consider the cost, benefit and risk appraisals for each option.

The information in the Business Case is necessary to assess the balance between the development, operational, maintenance and support costs against the financial value of the benefits over a period of time, in order to achieve an informed business commitment to the project.

This is often termed an investment (or cost/benefit) appraisal and the figures are normally profiled over a fixed number of years, or the useful life of the project’s products.

Corporate or programme management may have prescribed accounting rules defining how the investment should be appraised.

The Project Board needs to ensure that the benefits cited are aligned to any related strategic and/or programme initiatives planned.

The baseline for investment appraisal is usually the ‘do nothing’ option, i.e. the picture of the likely costs and benefits if the project is not undertaken.

If circumstances dictate that ‘something must be done’ (e.g. imminent new legislation), the baseline might instead be ‘do the minimum’.

Whichever baseline applies, it should be used for comparison with the expected outcome of the ‘recommended’ project option.

Wherever possible, benefits should be expressed in tangible ways.

To start with, the customer, user or Executive may define many benefits as intangible - for example, ‘happier staff’.

For a large investment, benefits should be expressed in more tangible ways.

In this example, ‘happier staff’ may translate into lower staff turnover and/or less time off for stress-related problems.

Both of these can be converted into a likely financial saving.

A factor that often occurs when a project involves a commercial agreement between more than one organization is that the customer and supplier have independent Business Cases for the investment, reflecting their own business interests.

In this case, the Executive must clarify and champion the Business Case on behalf of corporate or programme management.

All references above are in Directing Successful Projects with PRINCE2 unless stated otherwise.

PRINCE2® is a Registered Trade Mark of the Office of Government Commerce in the United Kingdom and other countries.

Managing Successful Projects with PRINCE2 - 2005 edition

Managing successful Projects with PRINCE2 – 2009 edition

Directing Projects with PRINCE2.

plus:

The Complete Project Management package.

And much more besides - at a fantastic price.